Budget Basics for PTOs

Budgeting makes all of your financial decisions easier. Follow these steps to create a budget for your PTO, even if you’ve never had one before.

The benefits of an annual budget are numerous. Having a budget helps your group prioritize its spending and lets you know whether your group has earned enough to do everything it wants to. It gives your group the flexibility to spend money while at the same time maintaining control over how it gets spent.

It’s well worth the development time to give your members confidence that their hard-earned fundraising money will be spent in ways they approve. Even if your group has never had a formal budget, your executive board in general and the treasurer in particular can prepare one to meet your needs. When you set a budget at the start of the school year, your school’s staff members and principal know what level of financial support they can expect from the PTO, and they can plan accordingly. And your individual officers aren’t burdened with the personal responsibility of deciding the best way to spend the PTO’s funds from request to request.

Reviewing Previous Financial Activity

If your PTO has been in existence for at least one year and you use a checkbook, you have the information you need to develop a budget. The actual financial activity of your group is recorded in the checkbook. All you need to do is review it and classify it. Your goal in conducting a checkbook review is to figure out how and where the PTO earned and spent its money for the year. With that information, you can tweak the numbers to get a plan for next year.

Join the PTO Today community (it's free) for access to resources, giveaways and more

Review at least one year’s worth of checkbook activity. If you can, conduct the review for two or three years. This additional effort will uncover any odd situations that do not occur on a regular basis. You want to avoid making budget decisions based on flukes.

As you go through your checkbook for the year, consider each individual entry. Is it a deposit or a check written? Deposits represent income; checks represent expenses. To make this analysis easier, you might want to copy your budget file (or, if you’re using a paper check register, photocopy all the pages) so you can make notes.

Deposits Made (Income)

The deposits made into your checking account can probably be grouped into five to seven sources of income. For example, you might have made three large deposits as part of your major gift-wrap fundraiser. All three checkbook entries are related to the fundraiser.

Let’s assume your PTO will conduct the same fundraiser next year. Thus, the gift-wrap fundraiser becomes one income category in your new budget. The amount of money you assign to the new fundraiser budget should be based on how much you actually collected last year.

Continue to review all the deposits made last year, looking for other logical groupings to create your PTO’s income categories. Other examples might be membership dues, minor fundraiser, loyalty programs, and direct donations. If you model your income plans on last year’s deposits, you’ll create a sound budget based on your parent group’s actual history.

Checks Written (Expenses)

Your checkbook will have many entries for checks written. Each check applies to some category of expense for the PTO. If you review the entire year and group all the check entries into 10 to 20 expense categories, you’ll have figured out how the group spent its money last year. Knowing how money was spent in the past provides you the information you need to plan for next year.

When defining your expense categories, you can be as broad or as specific as you think is necessary, but keep these guidelines in mind:

-

If you create only a few very broad expense categories, each with a large percentage of the budget, your members will need to vote several times throughout the year on how to disperse these large budgets into different projects. This type of planning won’t provide the maximum benefit of creating a budget.

-

On the other hand, if you only set up many narrowly defined categories, each with a small budget amount, you might find the budgets too inflexible. With such tight restraints, you might be voting every month to move money from one category to another.

Somewhere in between is a happy medium. Talk to your principal and last year’s officers. Use their experience to help decide which projects should be budgeted individually and where larger, more broadly defined expense categories would be more appropriate.

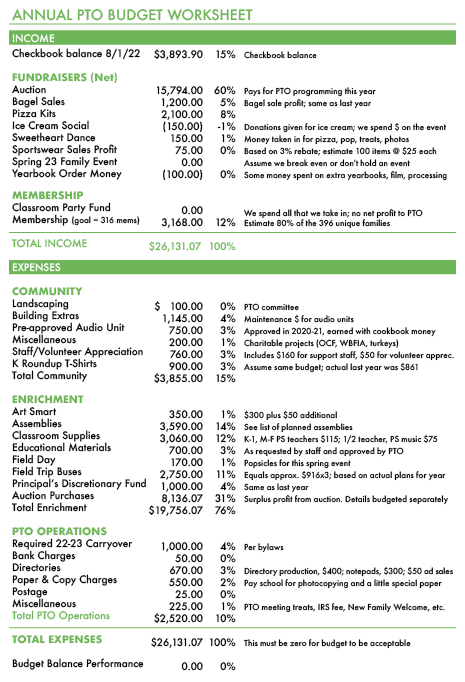

Generally, you can budget tightly for expenses when the amount is fairly predictable. For example, in the sample budget below, we calculated that we will spend $2,750 on field-trip buses. This amount is based on the actual transportation cost of three all-school field trips.

Conversely, in our sample we allocated $1,145 for “building extras.” At the start of the school year, we don’t know exactly how that money will be spent, but the principal knows she can receive that much money from us for extra physical items for the building. By allocating a portion of our budget into a few broad categories, we retain some flexibility but still maintain control.

Finding Balance

Look over the distribution of your total spending budget. If you have more than 20 percent in any one category, you might want to consider breaking down the category further to make the budget more manageable.

After you decide what expense categories to use, assign last year’s actual checks to the appropriate category. Don’t worry too much about tracking to the penny. Your goal here is simply to get a general idea of how much money was spent in each of the expense categories. When you’ve reviewed the entire past year, you’re ready to create the plan for the new school year.

List your new income and expense categories on a spreadsheet, as in the sample. The first income category should be your current checkbook balance, because that is, in essence, a source of income for your PTO. Follow that with all the categories for income generation and then all the expense categories you defined.

If your bylaws require that a minimum amount of money be carried into the following school year, list that amount as an expense category. Next to each category on your spreadsheet, fill in the amount based on your checkbook review. Look over the list of categories. Are there any new projects planned for next year that don’t show up yet? If so, add categories as necessary. Also consider whether you can use a logical calculation to determine an even better number for some of your categories. For example, bagel bakery costs might be based on $87 per week for 34 weeks, a total of $2,958.

Now comes the fun part. Adjust the amount of each category to get the total income to equal the total expenses without departing too far from the numbers you collected from your checkbook review. As you work, jot down the assumptions you’re making so you can explain your reasoning later.

Keep tweaking until you’re satisfied with the results and your budget is balanced. It’s vital that the total income exactly equal the total expenses so that your budget is balanced. If your income is higher than your expenses, find a way to spend more money, even if it’s to set it aside into a “Future Projects” category. On the other hand, if your expenses exceed your income, you must either cut back on expenses or come up with a way to make more money.

Get your executive board and principal to review and approve the budget before you present it to your membership for approval. Come to your meeting prepared with the budget spreadsheet handout and your notes so you can explain the assumptions you made. With your members’ approval secured, the PTO is “open for business” and you deserve a pat on the back.